The Surreal World of Money

What’s your favorite coin? Is it a refined, delicate, and dignified Roosevelt dime? A useless but comfortingly familiar Lincoln penny? The ubiquitous Washington quarter?

I prefer silver dollars, but not recent ones—they look and feel too much like quarters.

I like Eisenhower dollar coins, which were minted from 1971 to 1978. Their large size—a full 1.5 inches across—makes them distinctive and readily identifiable in your pocket, if you still carry coins. And their design acknowledged the 1969 moon landing with an engraving of an eagle landing on the moon and the earth in the distance, which is pretty cool.

But my all-time favorite is the Morgan dollar, which was minted from 1878 through 1904 and again (briefly) in 1921. It’s one of the few American coins to have been minted in five different cities: Philadelphia, New Orleans, Denver, Carson City, and San Francisco. (These days only the Denver and Philadelphia mints produce coins for circulation.) An astonishing 657 million Morgan dollars were created. Best estimates suggest that only about 1.4 million coins survive; sadly, most of the others have been melted down.

Designer and engraver George T. Morgan, after whom the coin is named, gave it a classically elegant design, with a woman’s profile on the face of the coin that represents liberty. The model was Philadelphia schoolteacher Anna Williams, who Morgan thought had a “nearly perfect Grecian profile.” Thirteen stars represent the original 13 colonies, and “E pluribus unum” reminds us of safety in numbers. The Morgan dollar has a classic bald eagle design on the back, replete with arrows and olive branches in the bird’s talons, representing war and peace. The words “In God we trust” are emblazoned above the eagle’s head. Apparently the Almighty also endorses coins.

The Morgan dollar is the most popular coin ever made in the United States, and it is easy to see why. It’s big—1.5 inches in diameter—and it has heft—weighing in at 26.73 grams. Each one is 90 percent silver and 10 percent copper, so you know that you are holding nearly an ounce of the semiprecious metal in each coin. By contrast, paper money—and monetary exchanges through the use of debit and credit cards, electronic transfers, or smart phones—seem entirely arbitrary and abstract, if not ethereal. (Don’t get me started on the intangible digital currencies like Bitcoin.)

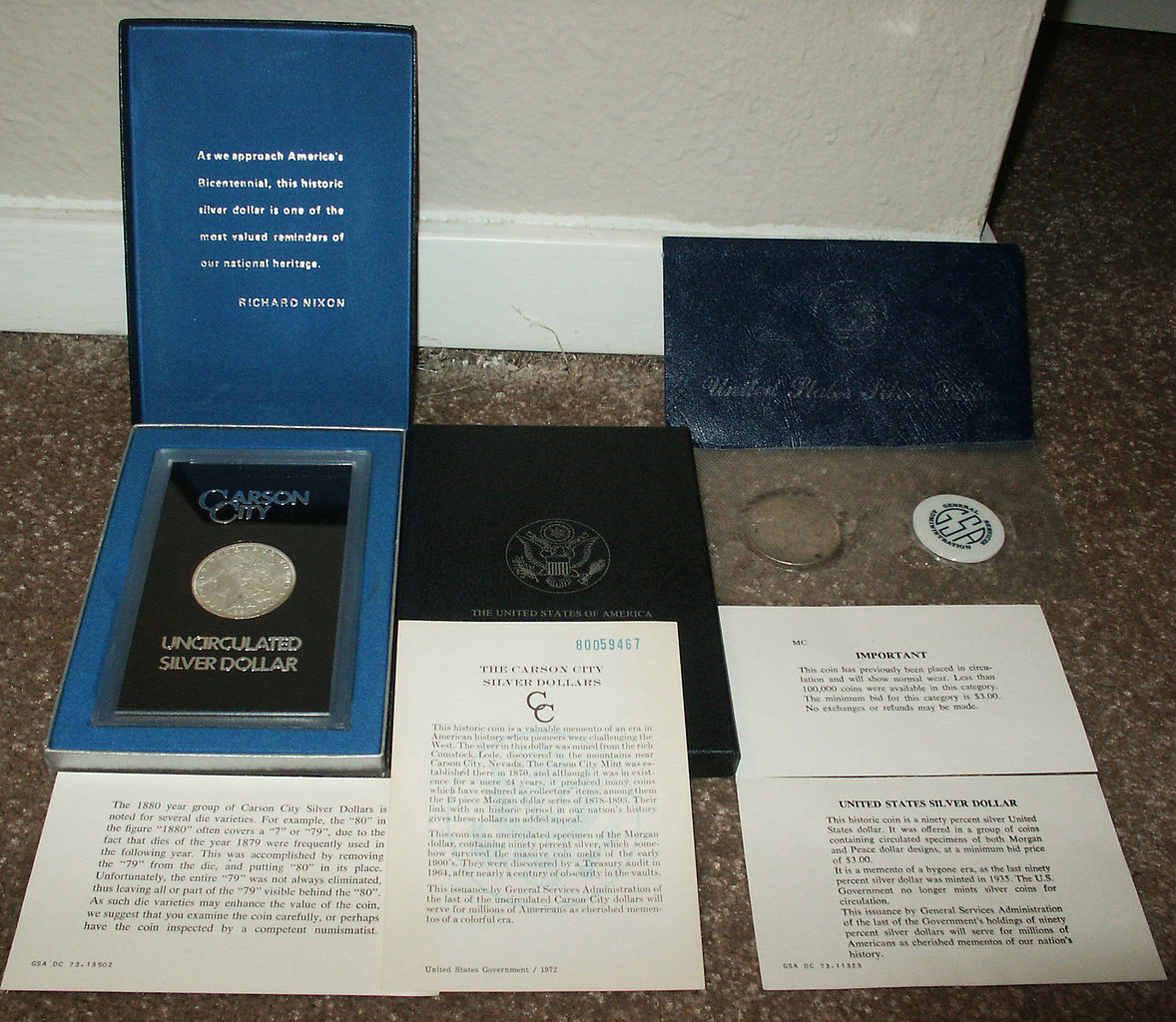

My favorite Morgan dollar is the 1884 series, minted in Carson City, Nevada. In the mid-1970s, when I was 9 years old, the Government Services Administration auctioned off several million Morgan dollars that had been in storage for nearly a century. With money I saved from my allowance, I purchased an uncirculated 1884 Carson City Morgan dollar for US$40. It arrived at my house in a large plastic case with a black background. “Carson City” was written in bold silver lettering above the coin and “Uncirculated Silver Dollar” was printed below it. I treasured that coin, for I was just beginning to fall in love with the American West, and Carson City was about as western as it got for a city boy from Chicago who didn’t know any better.

My infatuation with currency didn’t stop there—fast-forward to high school, when I went camping with several friends at the Indiana Dunes National Lakeshore not far from Chicago. We set up our smelly, eight-person canvas tent, ate some food, and then went for a swim in Lake Michigan.

A gentle wind was blowing in from the south, off the dunes and out over the lake. As a result, there were no waves at all—the lake was as smooth as glass.

We waded out into deeper water. We were in up to our chests when one of my friends realized that he still had his wallet in his pocket. He found three bills in it: a US$1, a US$5, and a US$20. For some reason, he pulled them out and laid them gently on the surface of Lake Michigan, where they floated motionless.

We stared at the money, removed from all pretense of its normal context, for what seemed like an eternity. One person serenely wondered aloud: “Why is this bill worth 20 times that one?”

Someone else said, “Why is this one worth five times that one?”

Then another chimed in: “That one is worth four times that one but 20 times this one. Why?”

It was a surreal moment and remains an extraordinary memory: Four 17-year-olds contemplating the theory of money while standing chest deep in smooth-as-glass Lake Michigan. We never came up with reasonable or sensible answers to our questions, but I never forgot the fact that we asked them.

More than three decades later, I still don’t have answers to those questions. The best I can do is throw my hands up in the air and say “trust”—trust in the federal government to do its best to maintain a symbolic relationship between people, paper bills, products, commodities and services, and symbols. The abstract nature of these connections brings me back to the Morgan dollar.

During much of the Morgan dollar’s run, most Americans preferred to use paper money instead of bulky coins, especially people who lived in urban areas and on the coasts. As a result, the Morgan dollar was primarily circulated in the American West, where people still preferred to carry coins.

If you had Morgan dollars in your pocket, you knew you had money in the bank, as it were. An 1884 coin, when its value is adjusted for inflation, would have been worth roughly US$27 in 2016, more than any of the bills we discussed at Indiana Dunes National Lakeshore.

The Morgan dollar was a force to be reckoned with. You knew it when you got paid. If worse came to worst, you could always melt the coins down for their silver content. Paper money and credit cards don’t seem as tangible—the paper and plastic out of which they are made is basically worthless—and therefore don’t seem as real, at least to me.

Today, the beleaguered Lincoln penny isn’t worth the metal it’s printed on, and the Jefferson nickel isn’t far behind. And I never carry US$26 in my pocket, even if I do want to discuss the theory of money! Times have indeed changed.

As a member of modern American society, I have no choice but to trust that the government will ensure that the arbitrary combination of ink, symbols, and phrases it prints on the rectangular pieces of paper it issues will continue to mean something—and something consistent.

And I have to assume that my bank guarantees that the arbitrary combination of bits and bytes created by my keystrokes mean something consistent as well.

At the end of the day, is it true that all I can do is trust in symbols?

That strange day in Lake Michigan no longer seems so anomalous. The meaning of money is wonderfully elusive.